Appointed Insurance Agency: Chong Hing Bank Limited, OCBC Wing Hang Bank Limited, Shanghai Commercial Bank Limited and Wing Lung Bank Limited

Give You a Prosperous Future

Maybe you are satisfied with your status quo, you still have to prepare a more prosperous future or retirement life for you and your beloved family. Monthly Income Protection Plan (The "Plan") offers not only a maximum of 15 years Guaranteed Monthly Income, but also a lump sum of Guaranteed Bonus by the commencement of the Income Period, enabling you to establish strong financial planning with ease.

Short Premium Payment Term Provides Flexible Options

The Plan provides 3 types of Premium Payment Term, i.e. 3 years, 5 years and 10 years1, plus different Accumulation Period and Income Period to suit your needs.

| Monthly Income 6 | Monthly Income 10 | Monthly Income 15 | |

|---|---|---|---|

| Premium Payment Term | 3 Years | 5 Years | 10 Years |

| Accumulation Period | 6 Years (1st to 6th Policy Year) |

10 Years (1st to 10th Policy Year) |

15 Years (1st to 15th Policy Year) |

| Income Period | 6 Years (7th to 12th Policy Year) |

10 Years (11th to 20th Policy Year) |

15 Years (16th to 30th Policy Year) |

| Benefit Term | 12 Years | 20 Years | 30 Years |

Monthly Income2 Brings You No Worries

You may decide the specific amount of Guaranteed Monthly Income payable during the Income Period to fit your personal needs. Besides, the Plan may provide extra Non-guaranteed Monthly Income3 to enhance the potential return of the Policy. You can choose cash withdrawal of the Guaranteed Monthly Income and Non-guaranteed Monthly Income3 every month or leaving them with the Policy for interest accumulation4. If accumulation with interest4 at the Policy is chosen, you may withdraw them anytime or upon Policy Maturity according to your personal needs.

Guaranteed Bonus for More Flexibility

By the commencement of the Income Period, a lump sum of Guaranteed Bonus will be paid for you to start your retirement. You may choose cash withdrawal or leaving it with the Policy for interest accumulation4.

| Monthly Income 6 | Monthly Income 10 | Monthly Income 15 | |

|---|---|---|---|

| Guaranteed Bonus | Guaranteed Monthly Income x 12 | Guaranteed Monthly Income x 18 | |

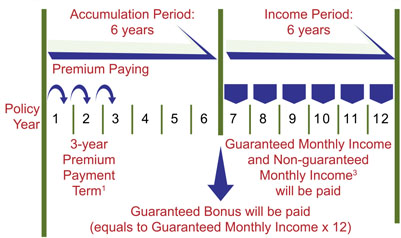

Example:

The Premium Payment Term of Monthly Income 6 is as short as 3 years1. The Guaranteed Bonus will be paid on the 6th Policy Anniversary. Starting from the 7th to 12th Policy Year, the Guaranteed Monthly Income and Non-guaranteed Monthly Income3 will be paid:

Enjoy Additional Return

Annual Dividend (non-guaranteed)5 may be distributed annually. During the Accumulation Period, the Annual Dividend (non-guaranteed)5 will be distributed in terms of cash, you may choose cash withdrawal, leaving it with the Policy for interest accumulation5 or premium reduction to meet your personal needs. During the Income Period, the full amount of Annual Dividend (non-guaranteed)5will be left with the Policy for interest accumulation5. The total amount of distributed Annual Dividend left with Hong Kong Life and its accumulated interest (non-guaranteed)5 will then be used to pay for the Non-guaranteed Monthly Income3.

Life Protection for Peace of Mind

If the Life Insured dies while the Plan is in force, the Total Death Benefit will be paid to the Policy Beneficiary.

|

Total Death Benefit |

|

|---|---|

| Within the Accumulation Period | During the first 2 Policy Years: 102% of Total Premiums Paid OR 100% of Guaranteed Cash Value as at the date of death of the Life Insured (whichever is greater), plus Accumulated Dividends and Interest (non-guaranteed)5,6 (if any), less Indebtedness (if any). Starting from the 3rd Policy Year: 105% of Total Premiums Paid OR 100% of Guaranteed Cash Value as at the date of death of the Life Insured (whichever is greater), plus Accumulated Dividends and Interest (non-guaranteed)5,6 (if any), less Indebtedness (if any). |

| Within the Income Period | 100% of Guaranteed Cash Value as at the date of death of the Life Insured, plus Accumulated Guaranteed Bonus (if any), Accumulated Guaranteed Monthly Income (if any) and Accumulated Dividends and Interest (non-guaranteed)5,6 (if any), less Indebtedness (if any) |

Fixed Premium for Your Better Planning

The premium rate will remain unchanged throughout the Premium Payment Term allowing you to have a better plan for your future.

Simple Application

Application procedure is simple and no medical examination is required.

Flexible Choice of Rider7 to Meet Your Needs

You may enhance your coverage by attaching different riders7 to the Policy including Waiver of Premium Benefit7 and Payor Benefit7 to fit your personal needs.

| Monthly Income 6 | Monthly Income 10 | Monthly Income 15 | |

|---|---|---|---|

| Premium Payment Term | 3 Years | 5 Years | 10 Years |

| Issue Age* | Aged 0 (15 days after birth) to 65 | Aged 0 (15 days after birth) to 60 | |

| Policy Currency | HKD / USD | ||

| Benefit Term | 12 Years | 20 Years | 30 Years |

| Minimum Guaranteed Monthly Income | HKD800 / USD100 | ||

| Maximum Total Premiums Paid | HKD20,000,000 / USD2,500,000 | ||

| Premium Payment Mode | Annual / Semi-annual / Quarterly / Monthly | ||

*Age means age of the Life Insured at the last birthday

- The Policy will be terminated if the Policyowner cannot settle the premium payment before the end of the Grace Period during the Premium Payment Term, subject to the Automatic Premium Loan, Non-forfeiture Option and other relevant provisions of the Policy. For detailed terms and conditions, please refer to the policy document issued by Hong Kong Life. If the Policy is terminated before the Policy Maturity, the Total Surrender Value (if applicable) received by the Policyowner may be less than the Total Premiums Paid.

- Monthly Income includes Guaranteed Monthly Income and Non-guaranteed Monthly Income.

- Non-guaranteed Monthly Income is not guaranteed and may be changed from time to time. Past performance is not indicative of future performance. The actual amount received may be higher or lower than the estimated amount. Hong Kong Life reserves the right to change it from time to time.

- The annual interest accumulation rate is not guaranteed and may be changed from time to time. Past performance is not indicative of future performance. The actual amount received may be higher or lower than the estimated amount. Hong Kong Life reserves the right to change it from time to time.

- Annual Dividend and the annual interest accumulation rate are not guaranteed and may be changed from time to time. Past performance is not indicative of future performance. The actual amount received may be higher or lower than the estimated amount. Hong Kong Life reserves the right to change them from time to time. The Annual Dividend and/or interest withdrawn will no longer be accumulated as part of the Total Surrender Value and the Total Death Benefit of the Policy. The Total Surrender Value and the Total Death Benefit of the Policy will be reduced accordingly.

- Accumulated Dividends and Interest means the aggregate of (1) the total amount of distributed Annual Dividend and Non-guaranteed Monthly Income left with Hong Kong Life (if any); and (2) the total amount of interest accumulated on any distributed Annual Dividend, Guaranteed Bonus, Guaranteed Monthly Income and Non-guaranteed Monthly Income left with Hong Kong Life.

- Only applicants who are defined as standard class applicants are accepted. Application for riders must comply with the issue age requirement of the riders and are subject to normal underwriting procedures. Riders can be applied together with the Plan or at each Policy Anniversary. Riders will be terminated simultaneously when the Plan is terminated. For details of riders, please refer to the policy document issued by Hong Kong Life.

Risk

Exchange Rate Risk

If the Policy Value and premium of the Plan are calculated in USD, all benefit amount will be presented in USD. If the benefit amount is received in terms of HKD, it is subject to the exchange rate between USD and HKD as determined by Hong Kong Life at the time of payment. Due to the potential fluctuation of the exchange rate, if USD depreciates substantially against HKD, the benefit value (calculated in HKD) of the Policy may be substantially decreased; if USD appreciates substantially against HKD, the premium (calculated in HKD) of the Policy may be substantially increased.

Liquidity Risk / Long Term Commitment

The Plan is designed to be held until the Maturity / Expiry Date. If you terminate the Policy prior to the Maturity / Expiry Date, a loss of the premium paid may be resulted.

The premium of the Plan should be paid in full for the whole payment term. If you discontinue the payment, the Policy may lapse and a loss of the premium paid may be resulted.

Credit Risk of Issuer

The Plan is issued and underwritten by Hong Kong Life. Your Policy is subject to the credit risk of Hong Kong Life. In the worst case, you may lose all the premium paid and benefit amount.

Market Risk

The amount of dividends (if any) of the Plan depends principally on the factors including investment returns, claim payments, policy persistency rates, operation expenses and tax; while the annual interest accumulation rate principally depends on the factors including investment performance and market conditions. Hence the amount of dividends (if any) and annual interest accumulation rate are not guaranteed and may be changed over time. The actual dividends payable and annual interest accumulation rate may be higher or lower than the expected amount and value at the time when the Policy was issued.

Inflation Risk

When reviewing the values shown in the Insurance Proposal, please note that the cost of living in the future is likely to be higher than it is today due to inflation.

Important Policy Provisions

Suicide

If the Life Insured commits suicide, while sane or insane, within one (1) year from the Issue Date or date of any reinstatement, whichever is later, the liability of Hong Kong Life shall be limited to a refund of paid premiums to the Beneficiary without interest less any existing Indebtedness. In the case of reinstatement, such refund of premium shall be calculated from the date of reinstatement.

This clause shall not apply to any Supplementary Benefit granting disability, accident or hospital benefits attached to the Policy unless stated otherwise in the contrary.

Incontestability

The validity of the Policy shall not be contestable except for (i) the non-payment of premiums, (ii) fraud or (iii) misstatement of age and/or sex as specified in the Misstatement of Age and/or Sex provisions, after it has been in force during the lifetime of the Life Insured for two (2) years from the Issue Date or date of any reinstatement, whichever is later. Premiums paid will not be refunded should the Policy be voided by Hong Kong Life.

This clause shall not apply to any Supplementary Benefit granting disability, accident or hospital benefits attached to the Policy unless stated otherwise in the contrary.

Automatic Termination

The Plan shall terminate automatically:

- upon the death of the Life Insured; or

- if and when the Plan matures or is surrendered; or

- if and when a premium remains unpaid at the end of the Grace Period as specified in the General Provisions unless Automatic Premium Loan applies; or

- if and when the Indebtedness of the Policy equals to or exceeds the Guaranteed Cash Value as shown on the Policy Schedule; or

- if and when the Guaranteed Cash Value as shown on the Policy Schedule less Indebtedness (if any) is less than the premium required to maintain the Policy up to the next premium due date as specified in the Automatic Premium Loan provisions.

Others

Insurance Costs

The Plan is an insurance plan with a savings element. Part of the premium pays for the insurance and related costs (if any).

Policy Fee

Part of the premium of the Plan pays for the Policy Fee, the current annual Policy Fee is HKD240 / USD30.

Cooling-off Period

If you are not satisfied with your Policy, you have a right to cancel it within the cooling-off period and obtain a refund of any premium(s) and levy(ies) paid (in the original payment currency) to Hong Kong Life without any interest. A written notice signed by you should be received by Hong Kong Life Insurance Limited at 15/F Cosco Tower, 183 Queen's Road Central, Hong Kong within the cooling-off period (that is, 21 days after the delivery of the Policy or issue of the Cooling-off Right Notice (informing you/your representative about the availability of the Policy and Expiry Date of the cooling-off period), whichever is the earlier). After the expiration of the cooling-off period, if you cancel the Policy before the end of the term, the projected Total Surrender Value (if applicable) may be less than the Total Premiums Paid.

Dividends

Hong Kong Life determines the amount of divisible surplus that will be distributed in the form of dividends. Dividends will be determined and distributed according to the Policy's terms and conditions and in compliance with the relevant legislative and regulatory requirements as well as relevant actuarial standards, whereas Terminal Dividend is available for certain types of policies and payable at the termination of the policies.

The amount of divisible surplus depends principally on the factors including investment returns, claim payments, policy persistency rates, operation expenses and tax. Hence the amount of dividends is not guaranteed and may be changed over time. The actual dividends payable may be higher or lower than the expected amount at the time when the policies were issued. The withdrawal of dividends will decrease the Total Surrender Value and Total Death Benefit of the Policy.

Withdrawal of Cash Payments

The withdrawal of cash payments (including but not limited to guaranteed cash coupon (if any) and monthly incomes (if any) etc.) will decrease the Total Surrender Value and Total Death Benefit of the Policy.

Policy Loan

After the Plan has acquired a Guaranteed Cash Value and while the Policy is in force, the Policyowner may, upon the sole security and satisfactory assignment of the Policy to Hong Kong Life, apply for a Policy Loan from the Plan. Any loan on the Policy shall bear interest at a rate declared by Hong Kong Life from time to time. Interest on the loan shall accrue and compound daily from the date of loan. The Policy Loan Interest Rate is not guaranteed and will be changed from time to time. The loan and the interest accrued thereon shall constitute Indebtedness against the Policy. Interest shall be due on each Policy Anniversary subsequent to the date of loan. In the event that the Indebtedness of the Policy equals to or exceeds the Guaranteed Cash Value as shown on the Policy Schedule, the Policy will terminate. Any Policy Loan and accrued loan interest may reduce the Total Surrender Value and Total Death Benefit of the Policy.

No Policy Loan is allowed on or after the date of commencement of the Income Period.

Non-Protected Deposit

The Plan is not equivalent to, nor should it be treated as a substitute for, time deposit. The Plan is not a protected deposit and is not protected by the Deposit Protection Scheme in Hong Kong.

Dispute on Selling Process and Product

Chong Hing Bank Limited, OCBC Wing Hang Bank Limited, Shanghai Commercial Bank Limited and Wing Lung Bank Limited (collectively "Appointed Insurance Agencies" and each individually "Appointed Insurance Agency") are the Appointed Insurance Agencies of Hong Kong Life, and the insurance product is a product of Hong Kong Life but not the Appointed Insurance Agencies. In respect of an eligible dispute (as defined in the Terms of Reference for the Financial Dispute Resolution Centre in relation to the Financial Dispute Resolution Scheme) arising between the Appointed Insurance Agency and the customer out of the selling process or processing of the related transaction, Appointed Insurance Agency is required to enter into a Financial Dispute Resolution Scheme process with the customer; however any dispute over the contractual terms of the life insurance product should be resolved between Hong Kong Life and the customer directly.

The above information is for reference and is applicable within Hong Kong only. For terms and conditions, please refer to the policy document. If there is any conflict between the above information and the policy document, the latter shall prevail. The copy of the policy document is available upon request. Before applying for the insurance plan, you may refer to the contents and terms of the policy document. You may also seek independent and professional advice before making any decision.